Or watch the video

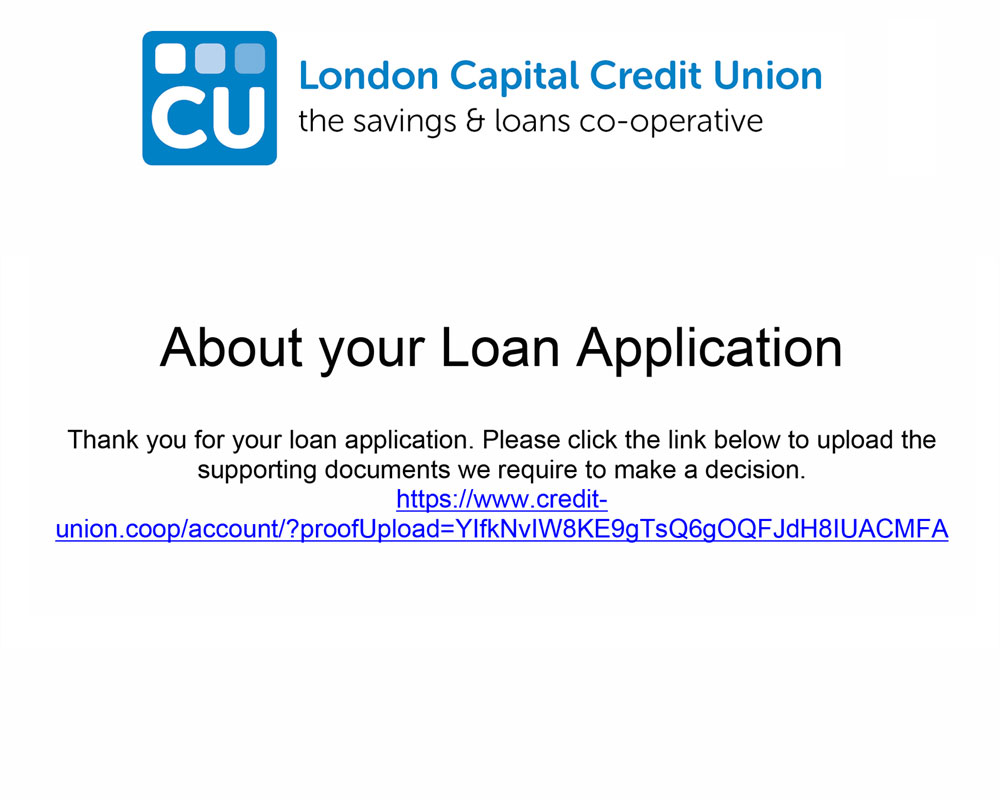

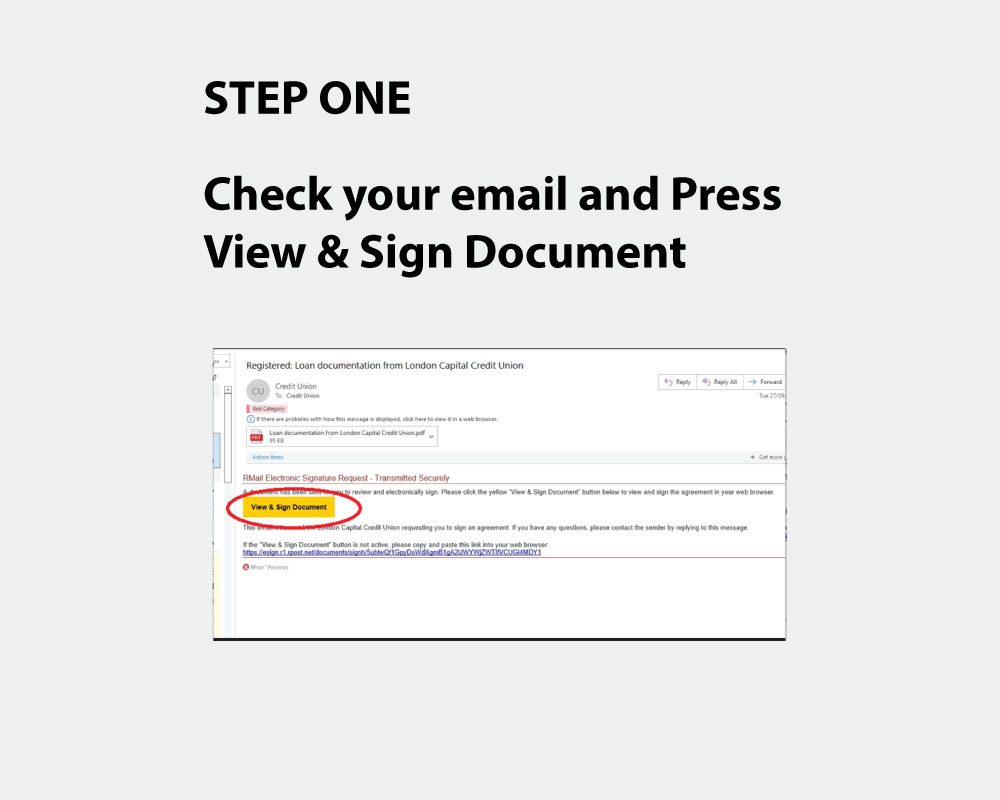

1. Click on the link in the email and text sent to you.

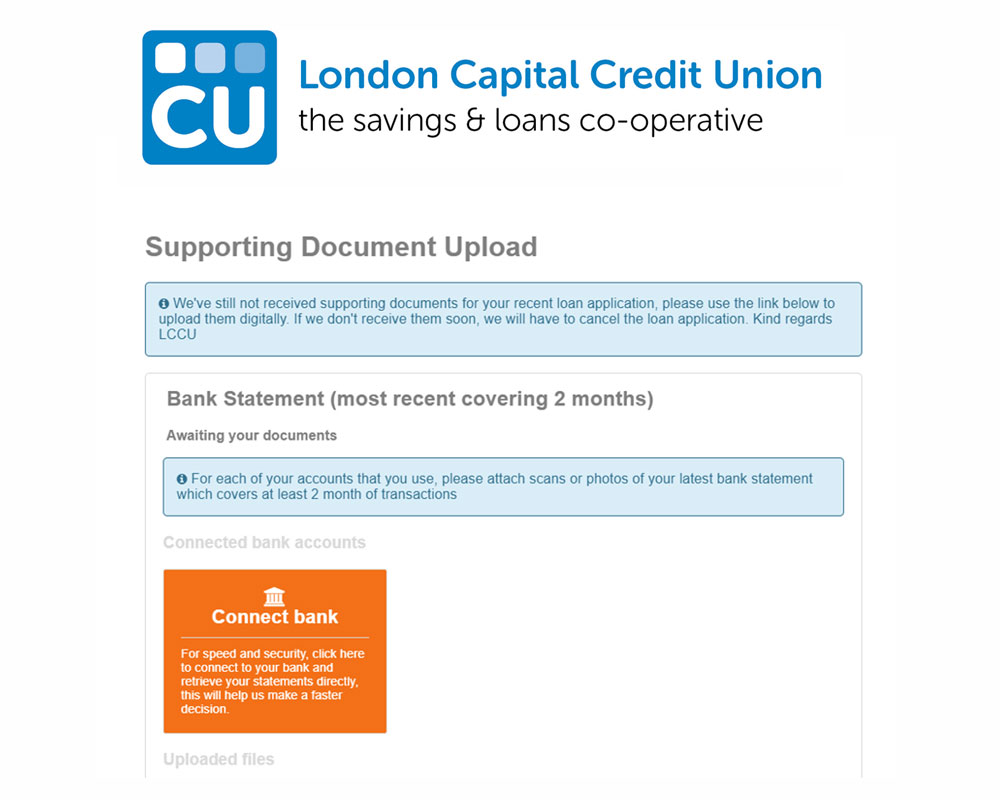

2. Click Connect Bank

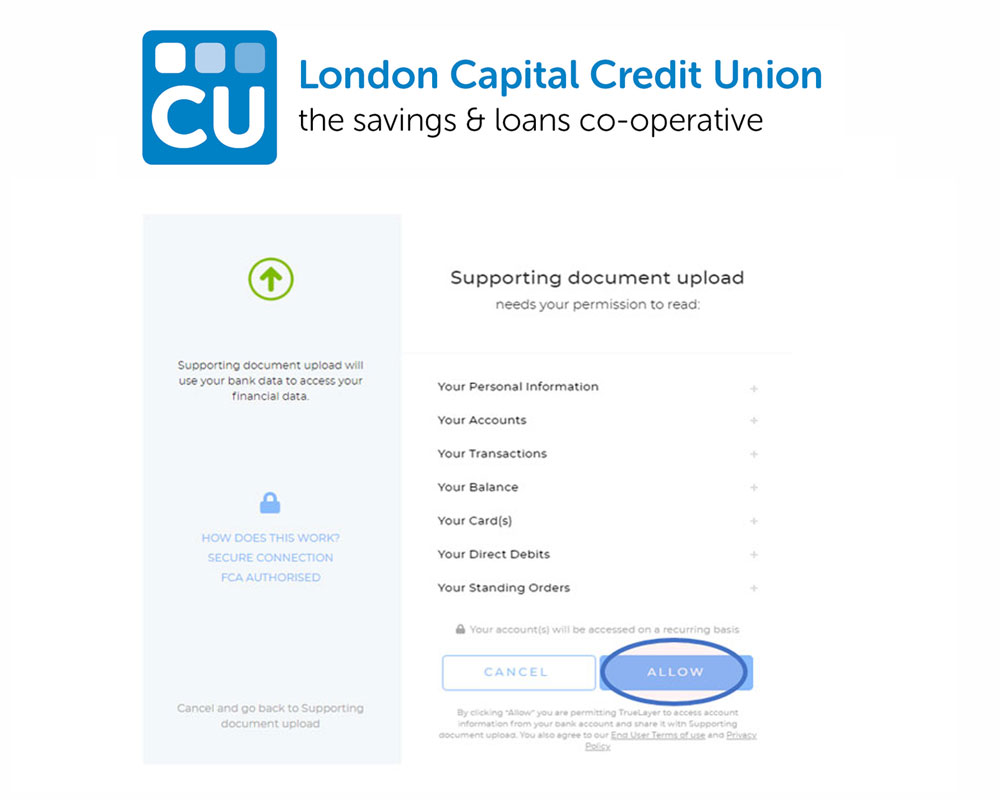

3. Click Allow

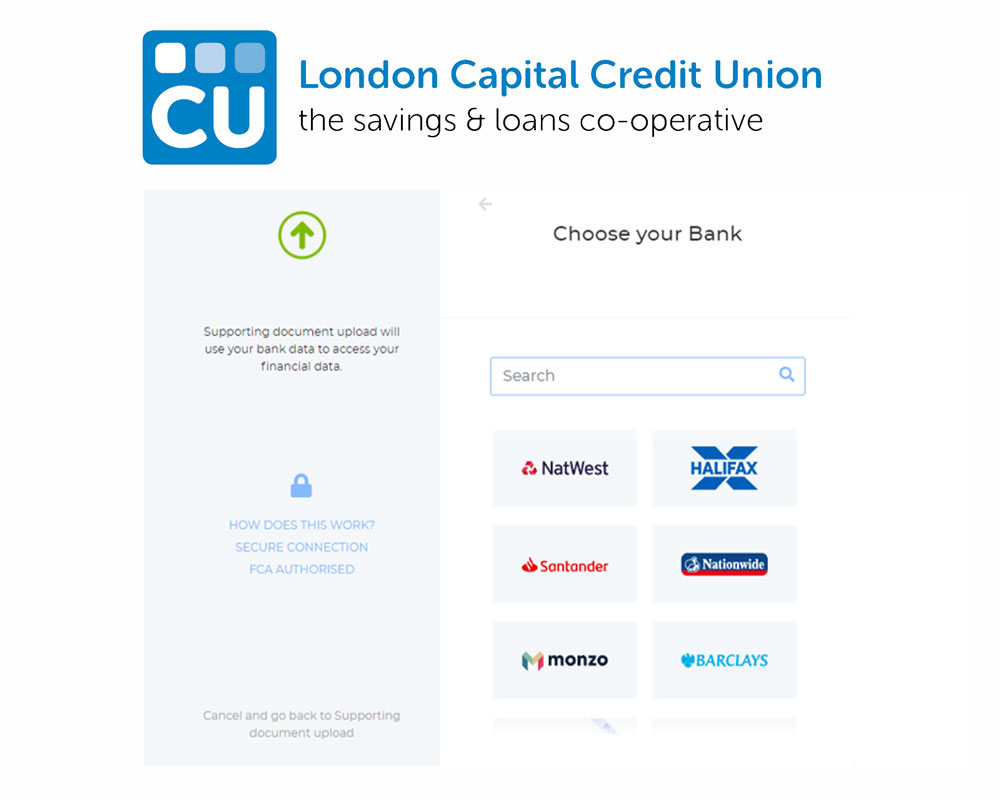

4. Select your bank through the list.

Metro bank and The Co-operative bank do not currently offer this option. If you bank with these providers you can email bank statements instead.

5. This will take you to your mobile / online banking ‘log in’ page.

Log in to your online banking and select all the accounts that you wish to connect. It will link statements with your loan application, when finished it will show pending from your side.

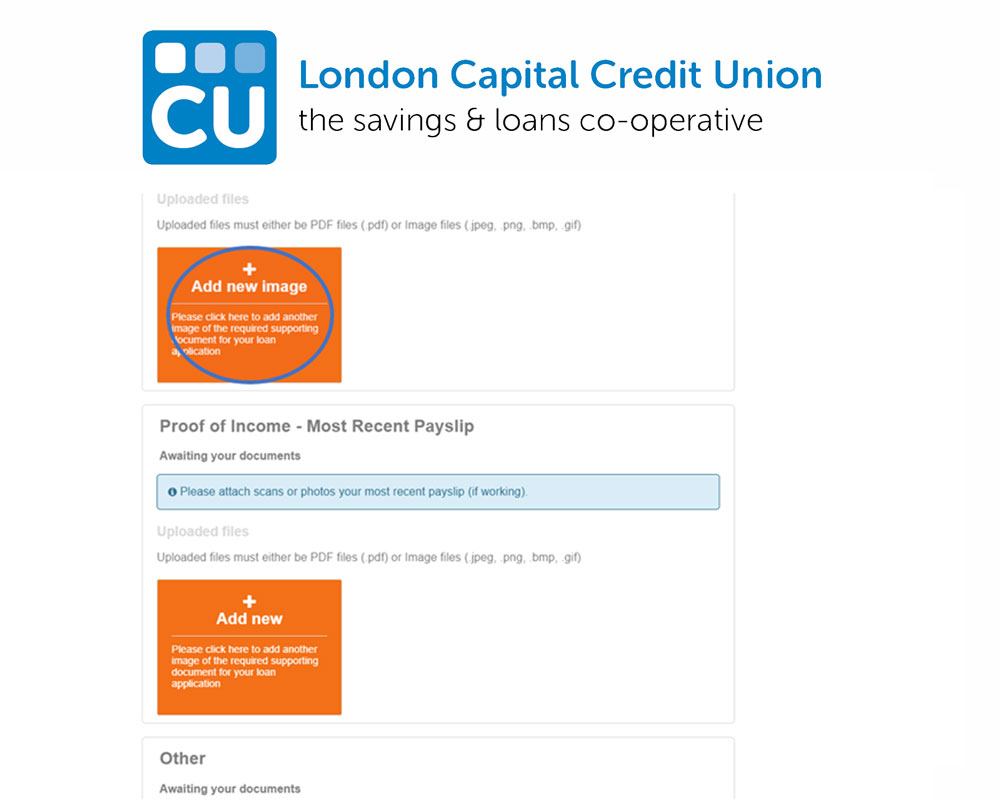

If you need to upload any additional documents or pictures, click on the add new image and upload documents as PDF or image files.

Or watch the video

Or watch the video